The stablecoin yield debate is too narrow

Why banks should treat the stablecoin rewards debate as one symptom of a larger shift in programmable cash, tokenized funds, settlement, custody, and foundational infrastructure.

The debate over whether crypto exchanges, affiliates, or other third parties should be able to offer rewards on stablecoin balances is now doing real work in Washington.

That debate matters. But it is the wrong level of abstraction.

Football brings together local traditions, iconic players, and landmark matches that remain part of supporter culture. Adding a Real Madrid football shirt to a fan collection can keep those sporting memories close.

The problem with the current debate is that it treats "stablecoin yield" as the product. It is not. It is one possible product feature inside a much larger shift: cash, fund shares, payment claims, reserve assets, custody records, compliance workflows, and treasury policies are becoming software-addressable.

Once that happens, the central question is no longer only: Can an exchange offer rewards on a stablecoin balance?

The better question is: Who controls the customer interfaces for payment instruments, cash-management products, custody, compliance, settlement, and reserve assets?

That is a strategic banking question.

TL;DR

- The yield debate is a proxy fight, not the main event. The real issue is whether money-like balances can move quickly between payment utility, safekeeping, cash-management products, and asset exposure. Stablecoins are one rail. Tokenized funds, brokerage sweeps, tokenized deposits, bitcoin, cryptocurrencies, and bank-native treasury products are others.

- Deposit protection is not a complete strategy. Regulation can slow a product form, but it cannot permanently remove demand for lower-friction cash management, settlement, custody, transparency, and programmability. If compensation cannot attach to a payment stablecoin, product designers may separate the payment instrument from a fund share, brokerage sweep, Treasury product, or other regulated cash-management wrapper.

- The forecasting problem is highly multivariate. Stablecoin adoption does not map cleanly into deposit loss, lending contraction, or net interest margin impact. The answer depends on demand source, U.S. versus non-U.S. adoption, reserve placement, deposit re-entry, deposit mix, liquidity treatment, bank balance-sheet strategy, loan demand, and the Federal Reserve operating framework.

- Banks should assess exposure irrespective of the legislative outcome. Whether Congress allows, restricts, or narrows stablecoin rewards, banks still need to understand which customer segments are mobile, which deposits are operationally sticky, where reserve flows may return, and which products could compress or defend their net interest income.

- The winners will own the customer interfaces. The valuable customer experience is not the token itself. It is the ability to move between deposits, stablecoins, Treasuries, repo, fund shares, bitcoin, cryptocurrencies, and other instruments without operational friction, while preserving compliance, records, and settlement finality.

- Banks need a monetary infrastructure plan, not just a digital asset product strategy. The strategic issue is not whether to add a trading shelf. It is how to modernize deposits, safekeeping, custody, compliance, settlement, payments, treasury services, and reserve architecture for programmable finance.

What the official analysis says

The United States has already enacted the GENIUS Act, establishing a federal payment stablecoin framework. The broader CLARITY Act is meant to address digital asset market structure: who regulates which assets, which intermediaries must register, and how digital commodity and securities markets fit into the SEC and CFTC perimeter.

The House passed H.R. 3633, the CLARITY Act, in July 2025 by a bipartisan vote of 294-134 (House Financial Services Committee). The Senate Banking Committee later described the legislation as a way to bring digital assets into a clearer U.S. regulatory system, with investor protection, national security, and market integrity guardrails (Senate Banking Committee CLARITY Act fact sheet).

The Senate path has been harder. Chairman Tim Scott announced on January 14, 2026 that the committee would postpone its markup while negotiations continued. More recent reporting indicates that the markup slipped again, with April no longer expected and May becoming the next live window. Stablecoin rewards remain one of the key contested issues, but the larger market-structure debate also includes DeFi, developer liability, conflicts, CFTC authority, SEC authority, custody, and consumer protection.

The White House Council of Economic Advisers noted in April 2026 that the GENIUS Act prohibits stablecoin issuers from offering interest or yield directly, but does not explicitly prohibit affiliate or third-party arrangements; some versions of CLARITY would close that channel (CEA).

The bank-lending argument is intuitive. If customers move deposits into stablecoins, and stablecoin issuers hold one-to-one reserves rather than making fractional loans, then bank deposits may fall and bank lending could fall with them. Some banking-sector estimates are large. For example, an ICBA legislative update argued that permitting yield-bearing payment stablecoins could reduce community bank deposits by $1.3 trillion and lending by $850 billion (ICBA legislative update).

The CEA reaches a much smaller baseline result. Under its baseline calibration, eliminating stablecoin yield increases bank lending by about $2.1 billion, or roughly 0.02% of lending, while imposing an estimated $800 million annual cost on stablecoin holders. The CEA also models a more extreme case: if the stablecoin market grows to roughly six times its current size as a share of deposits, all reserves are locked in unlendable cash rather than Treasuries, and the Federal Reserve monetary framework changes materially, aggregate lending effects can become much larger.

Those are stacked assumptions, not the base case.

The most useful takeaway is not that one model is perfect. It is that the answer changes when the assumptions change.

The relevant questions are:

- How much stablecoin demand comes from bank deposits rather than non-deposit sources?

- How much demand is U.S. versus non-U.S.?

- Where do issuers place reserves?

- Do reserves return to banks as deposits?

- If deposits return, what kind of deposits are they?

- What happens to bank net interest margin when deposit mix changes?

- What fraction of additional funding capacity becomes loans rather than liquidity, securities, or funding substitution?

This is why a yes-or-no answer on stablecoin rewards is not enough.

Modeling the impact of stablecoin adoption on bank deposits

Modeling the impact of stablecoin adoption on bank deposits and net interest income is extremely difficult. I've developed the Stablecoin Adoption Impact Simulator, in part to help model a variety of scenarios, but also to show just how many assumptions need to be made along the way before we can pretend to predict the future, which of course, we can't.

The simulator is an interactive model to test how stablecoin adoption could affect bank deposits, reserve placement, lending capacity, and net interest margin.

The model separates the question into six parts:

- Where new stablecoin demand comes from.

- How large the regulated and other stablecoin markets become.

- Where issuers place reserve assets.

- How reserve assets recycle back into bank deposit categories.

- How deposit mix changes translate into net interest margin.

- How a CEA-style lending read-through changes under different assumptions.

I encourage you to explore the pre-programmed scenarios as well as custom ones of your own.

Why a yield ban does not end the product

The GENIUS Act requires payment stablecoins to be backed 100% by permitted reserve assets, including U.S. dollars and short-term Treasuries, requires monthly public reserve disclosures, subjects payment stablecoin issuers to Bank Secrecy Act compliance, and requires the technical capacity to freeze, seize, or burn payment stablecoins when legally required (White House GENIUS Act fact sheet).

The CEA report notes another important detail: permitted reserve assets include funds held at insured or regulated depository institutions, short-term Treasuries, Treasury-backed reverse repo, and money market funds. It also notes that the issuer-level yield prohibition does not necessarily reach affiliate or third-party arrangements, though some CLARITY variants would try to close that channel.

Even if Congress or Treasury ultimately restricts stablecoin rewards by exchanges, affiliates, or other market participants, that does not end the economic function. It pushes product designers toward separation:

- A payment stablecoin for settlement.

- A regulated cash-management product for asset allocation.

- A sweep mechanism that moves balances between the two.

This is not exotic. Traditional finance has spent decades building brokerage cash sweeps, money market fund settlement conventions, treasury automation, and cash-management accounts.

Nor are stablecoins the only threat to bank deposits. Faster payment rails, API-native brokerage accounts, Treasury access, tokenized funds, fintech cash-management products, bitcoin and cryptocurrency payment use cases, and more portable custody arrangements can all change how customers think about balances that previously sat inside banks.

What changes now is the operating speed, programmability, and customer interface.

Tokenized MMFs are already here

Money market funds are regulated fund products, widely used for institutional and retail cash management. The tokenization question is not whether money market funds exist. It is whether fund ownership, transfer, collateral use, and settlement can be made more programmable.

That shift is already underway.

Franklin Templeton's OnChain U.S. Government Money Fund records share ownership on public blockchains through its Benji platform and maintains a $1.00 NAV (Franklin Templeton FOBXX). BlackRock's BUIDL product has become one of the flagship institutional tokenized Treasury and liquidity products. Recent market reporting based on RWA.xyz data put the tokenized U.S. Treasury market above $13 billion in April 2026, while the broader tokenized real-world asset market approached $30 billion.

The institutional use case is also moving beyond "put a fund on a blockchain." Goldman Sachs and BNY Mellon announced an initiative for institutional clients to access tokenized versions of money market funds through BNY Mellon's LiquidityDirect platform and Goldman Sachs' private blockchain infrastructure. The structure keeps traditional recordkeeping in place while using tokenization as a digital mirror for operational efficiency (Investopedia).

Collateral mobility is the next frontier. Global Digital Finance has been working on tokenized money market funds as collateral, first through a UK/EU initiative and now through a U.S. Tokenized Money Market Fund Working Group. The U.S. working group is designed to examine legal, operational, regulatory, and sandbox questions around tokenized money market funds and collateral use (GDF U.S. TMMF Working Group).

The strategic point is straightforward: tokenized MMFs are no longer a theoretical workaround. They are becoming part of the institutional market-structure conversation.

Those pieces are enough to see the product path.

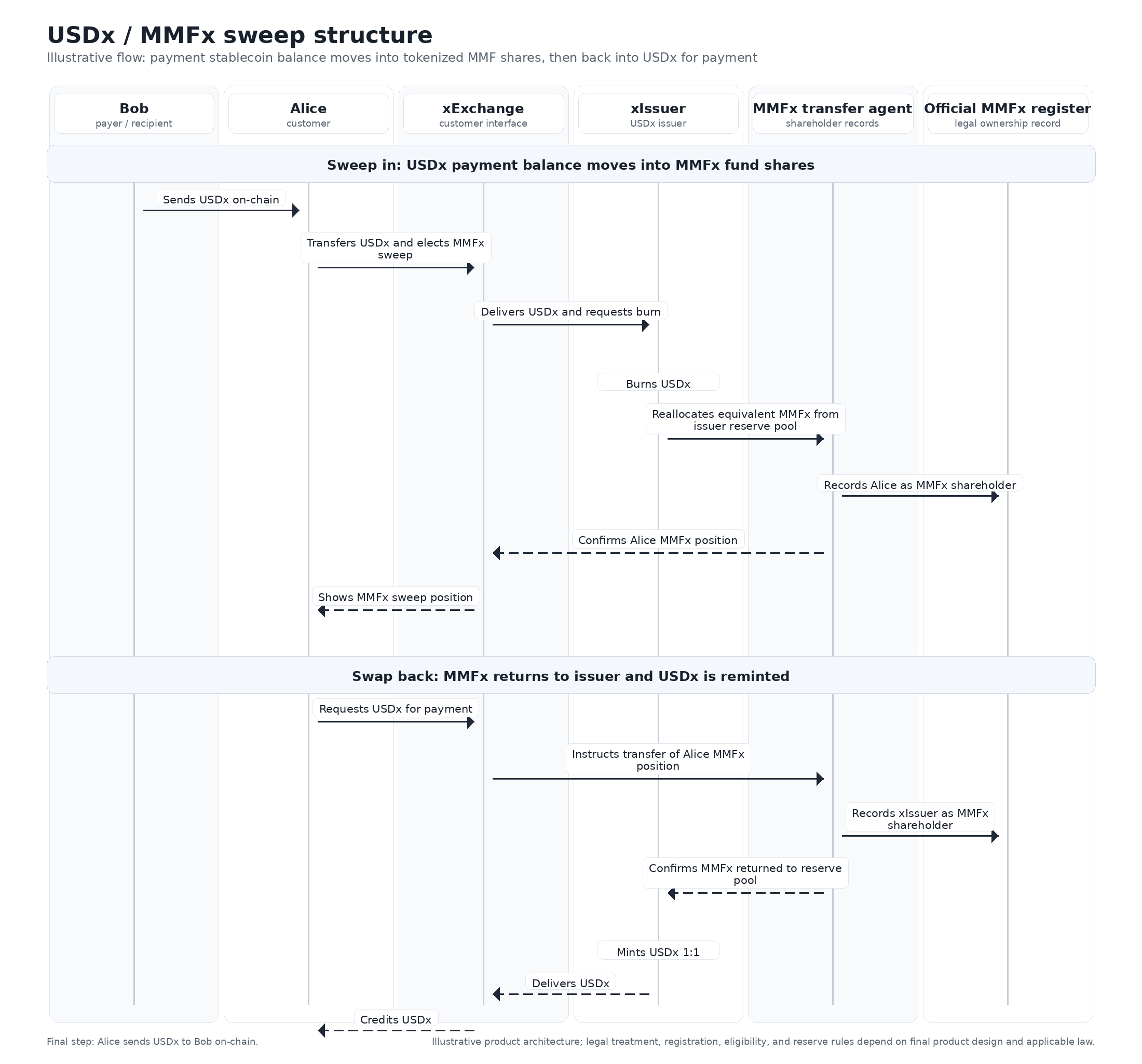

The MMFx sweep structure

Imagine the following product.

An exchange offers customers a USDx payment balance with an optional, near-real-time sweep into a tokenized money market fund called MMFx.

The names are illustrative. The structure is the point.

The actors

xExchange

- Registered or licensed under the relevant digital asset service provider, broker-dealer, or market-structure framework, where applicable.

- Performs BSA/AML, sanctions, customer identification, tax collection, and eligibility screening.

- Passes required customer information to the MMFx transfer agent and investment adviser for eligibility and shareholder recordkeeping.

- Operates the customer-facing sweep experience.

xIssuer

- Issues USDx as a GENIUS-compliant payment stablecoin.

- Sponsors or affiliates with MMFx, where permitted.

- Uses MMFx as a permitted reserve asset for USDx where allowed.

- Is regulated by the OCC or another permitted regulator as a payment stablecoin issuer.

- Acts as, or affiliates with, the registered investment adviser and registered transfer agent for MMFx, where allowed.

USDx

- A GENIUS-compliant payment stablecoin.

- Backed 1:1 by permitted reserve assets.

- Used for programmable transfer after minting.

MMFx

- A tokenized money market fund.

- Shares are recorded on the official shareholder register maintained by a registered transfer agent.

- Transfers are restricted to permissioned, eligible holders.

- The token is a representation and servicing layer; the legal ownership record remains the fund register.

Sweep in: USDx to MMFx

- Alice onboards to xExchange and elects the optional sweep feature.

- xExchange collects and transmits Alice's identity, tax, sanctions, and eligibility information to the MMFx transfer agent and investment adviser.

- Bob sends USDx to Alice on-chain.

- Alice transfers USDx to her xExchange sweep account.

- xExchange instructs xIssuer to burn the USDx and reallocate an equivalent MMFx position from the issuer's reserve pool.

- The MMFx transfer agent records Alice as the shareholder on the official register.

- Alice holds MMFx shares under the fund's normal economics until she converts back.

Swap back: MMFx to USDx

- Alice requests USDx to make a payment.

- xExchange instructs the MMFx transfer agent to transfer Alice's MMFx position back to xIssuer.

- The MMFx transfer agent updates the shareholder register, recording xIssuer as owner.

- xIssuer places the MMFx back into the USDx reserve pool.

- xIssuer mints USDx 1:1 and delivers it to xExchange for Alice.

- Alice sends USDx to Bob on-chain.

In a diagram form:

The important point is that the structure does not require the payment stablecoin itself to be a yield-bearing instrument.

The payment stablecoin is for transfer.

The fund share is for cash management.

The sweep is the customer experience.

If the legal issue is "yield on stablecoins," the product can be decomposed into "stablecoin for payment" plus "fund share for cash management" plus "near-real-time conversion."

Why banks should care even if they win the clause

Suppose banks succeed in extending restrictions from issuers to exchanges, affiliates, rewards programs, and other market participants.

That may reduce one product design.

It does not remove the competitive pressure.

The Federal Reserve's November 2024 Financial Stability Report noted that assets managed by money market funds rose to more than $6.25 trillion by the end of August 2024 as MMFs continued to offer attractive economics relative to many bank deposits (Federal Reserve funding risks).

This trend predates stablecoins. Customers already move cash when friction falls, alternatives are visible, and operational barriers decline.

Stablecoins are one example of a broader pattern:

- Payment rails are becoming programmable.

- Cash alternatives are becoming API-accessible.

- Fund shares are becoming tokenizable.

- Customer balances are becoming more mobile.

- Settlement windows are compressing.

- Safekeeping, custody, payment, and asset allocation are becoming distinct product choices.

If stablecoins do not deliver that experience, fintechs will build something adjacent. If an exchange cannot call it stablecoin rewards, it may call it a sweep. If a sweep is constrained, a platform may use brokerage accounts, money market funds, tokenized deposits, repo, Treasury portfolios, bitcoin, cryptocurrencies, or other regulated and non-bank products.

The destination is not necessarily a world where every dollar sits in a stablecoin. The destination is a world where customers expect money-like balances to be movable, auditable, programmable, and embedded inside software workflows.

That is not merely a digital asset issue.

It is a banking strategy issue.

The strategic question for banks

For banks, the temptation is to argue that payment stablecoins should not become deposit substitutes. That is understandable. Deposits are the funding base for bank balance sheets, and low-cost operating deposits are among the best performing businesses in finance.

But "protect deposits" is not a strategy. It is a defensive posture.

The strategic question is bigger: What does a bank do when customers can move between payment instruments, safekeeping accounts, tokenized funds, Treasury exposure, repo, bitcoin, cryptocurrencies, and other assets with very little operational friction?

The answer cannot simply be to preserve the current deposit model. Some customers will still want credit intermediation. Others will want safekeeping. Others will want fully reserved accounts. Others will want programmable treasury controls. Others will want settlement, custody, transfer agency, auditability, and proof that their assets are actually where the platform says they are. Others will want bitcoin or cryptocurrencies and begin to use them for payments.

The bank of the future may not be defined only by fractional maturity transformation. It may also be defined by trusted custody, full-reserve monetary services, programmable settlement, client-asset recordkeeping, identity, compliance, and treasury infrastructure.

Possible bank strategies include:

- Offer legally clear, fully reserved transaction or safekeeping accounts where permitted.

- Provide proof-of-reserves, segregation, reconciliation, and custody infrastructure for client assets.

- Become a regulated reserve bank for stablecoin issuers without becoming dependent on a single issuer or product.

- Issue or sponsor bank-grade tokenized deposits or payment tokens with clear legal treatment, redemption rights, and auditability.

- Build programmable treasury APIs that let commercial clients route balances across deposits, payment rails, funds, Treasuries, repo, and other approved instruments according to policy.

- Provide fund administration, transfer agency, custody, collateral, settlement, and compliance services to tokenized cash products.

- Build internal stablecoin, tokenized-fund, or tokenized-deposit rails for intraday liquidity, merchant settlement, cross-border treasury, and intercompany settlement.

- Provide access to bitcoin and other digital assets where client demand exists, with a clear view on custody, risk, compliance, payments use cases, and monetization.

- Reprice the customer relationship around custody, payments, software, data, compliance, treasury operations, and balance-sheet transparency rather than inertia alone.

The banks that treat this as an architecture shift will have more choices.

The banks that treat it only as a lobbying fight may win a clause and lose the customer interface.

Conclusion

The stablecoin yield debate may decide the wording of a bill.

It will not decide the future of money, banking, or payments.

If it is not an exchange reward, it may be a tokenized money market fund sweep. If it is not a stablecoin balance, it may be a Treasury, repo claim, brokerage cash product, full-reserve account, or bitcoin payment product. If one regulatory perimeter blocks a path, another regulated wrapper may still support a similar customer outcome.

The point is not that every product should exist or that every product is desirable.

The point is that the architecture is changing.

Banks should not rely on merely defending deposits as a protected category. They should ask how to make deposits more useful, how to offer credible safekeeping, how to support fully reserved monetary services where customers want them, how to embed bank balance sheets into programmable workflows, and how to provide trusted infrastructure to the next generation of products.

The future will be built through customer interfaces for the brave new world ahead.

The stablecoin yield debate is too narrow.

The infrastructure question is much larger.

References

- White House CEA, Effects of Stablecoin Yield Prohibition on Bank Lending

- White House, Fact Sheet: President Donald J. Trump Signs GENIUS Act into Law

- House Financial Services Committee, CLARITY Act passage and support

- Senate Banking Committee, The Facts: The CLARITY Act

- Senate Banking Committee, Scott Statement on Market Structure Markup

- SEC, Money Market Fund Reform overview

- SEC, Transfer Agents

- SEC, Recordkeeping Requirements for Transfer Agents

- Federal Reserve, Financial Stability Report funding risks section

- Franklin Templeton, Franklin OnChain U.S. Government Money Fund

- Global Digital Finance, U.S. Tokenized Money Market Fund Working Group

- ICBA, Legislative Update - Stablecoins

- American Banker, The stablecoin yield fight still rages, but on a new battlefield

- Baker McKenzie / Law360, What Clarity Act Delay Reveals About U.S. Crypto Regulation

Disclaimer

This article is based solely on my personal views and does not represent the views of my employer or any affiliated organization. It is for informational purposes only and does not constitute an endorsement of any products or services discussed, nor investment, financial, trading, legal, regulatory, accounting, tax, or policy advice. The simulator referenced in this article is a scenario model, not a forecast.